ATO NEWS

Government announces changes to proposed ‘Stage 3’ tax cuts

The Federal Government has announced tweaks to the ‘Stage 3’ tax cuts that will apply from 1 July 2024. The proposed changes are:

- reduce the 19% tax rate to 16%;

- reduce the 32.5% tax rate to 30% for incomes between $45,000 and a new $135,000 threshold;

- increase the threshold at which the 37% tax rate applies from $120,000 to $135,000; and

- increase the threshold at which the 45% tax rate applies from $180,000 to $190,000.

View more info, including a tax cut calculator, at the Treasury’s website here.

The Medicare levy low-income thresholds for the 2024 income year will also be increased.

Changes in reporting requirements for sporting clubs

Not-for-profits (‘NFPs’), including sporting clubs, societies and associations with an active ABN, need to lodge an annual NFP self-review return to continue accessing their income tax exemption. The main purpose of a sporting organisation must be the encouragement of a game, sport or animal racing. Any other purpose of the organisation must be incidental, ancillary or secondary. The organisation’s governing documents will help identify the purpose for which it was set up, and the organisation’s activities in the year of income must then demonstrate that the main purpose is the encouragement of its game, sport or animal racing.

NFP organisations need to lodge their first NFP self-review return for the 2024 income year between 1 July and 31 October 2024.

NFP organisations with their own ABN need to complete their own NFP self-review return even if they are affiliated with a broader sporting group.

If an NFP organisation does not lodge the return, they may become ineligible for an income tax.

Editor: If you need more information about this recent development, please contact our office.

Deductions denied for work-related expenses

The Administrative Appeals Tribunal (‘AAT’) recently held that a taxpayer should not be allowed deductions for various work-related expenses, largely because the substantiation requirements had not been satisfied. The taxpayer, a real estate salesperson, claimed tax deductions for the 2018 to 2020 income years, during which time he derived income from his employment with a real estate company. However, the ATO disallowed the taxpayer’s claims for various work-related expenses, including car expenses, and gifts and donations.

The AAT agreed with the ATO, and held that the expenses claimed were not deductible and that the taxpayer had failed to substantiate his claims. The taxpayer had claimed deductions for car expenses using the logbook method, but the AAT noted that the car was owned by a company and was not leased to the taxpayer. Therefore, the car was not ‘held’ by the taxpayer, as required by the logbook method. The taxpayer’s logbook also lacked “sufficient specificity” for this method.

While the taxpayer produced credit card statements and telephone tax invoices (about credit card interest and telephone expenses), it was not clear from these documents whether the costs claimed related to work expenses. The taxpayer sought to rely on bank transaction statements about other expenses, but they were considered to be insufficient, as it was unclear from these statements what the relevant expense was, how the expense was incurred in earning the taxpayer’s assessable income, and any apportionment between business and personal use. There were also no receipts or tax invoices for any of the claimed donations.

Sale of land subject to GST

The Administrative Appeals Tribunal (AAT) recently held that the sale of land by a taxpayer was subject to GST, as it was a supply made in the course of an enterprise being carried on by the taxpayer. The taxpayer purchased a single parcel of land in 2013 for $1.6 million, and he subsequently took steps for the land to be subdivided and rezoned. He then sold the land in 2021 for $4.25 million before the subdivision was completed. The ATO advised the taxpayer that the sale of the land was subject to GST as a taxable supply under the GST Act. The taxpayer objected to the GST assessment on the following grounds:

- the sale of the property was not made by him in the course of his enterprise; and

- as the property was the taxpayer’s residential premises, it was an input-taxed supply, so no GST should apply anyway.

However, the AAT agreed with the ATO that the sale of the property was subject to GST as a supply made in the course of the taxpayer’s enterprise. The AAT first noted that the sale of the property was not an input taxed supply of residential premises because the buildings on the property were uninhabitable, and so the property did not meet the definition of ‘residential premises’ in the GST Act. The AAT also held that the taxpayer’s development works were in “the form of a business”, even if he was not in the business of being a property developer. Relevant factors included the scale of the operations that the taxpayer was involved in (including rezoning and subdividing the property), as well as the amount of capital invested by him in the purchase of the property and development works. The taxpayer’s “series of activities” throughout his ownership of the property therefore amounted to the carrying on of an enterprise, and the taxpayer was liable to pay GST on the sale of the property.

Melbourne man sentenced to jail for attempting to defraud the ATO

A Wheelers Hill man was recently sentenced to three years and six months imprisonment for defrauding the ATO of nearly $35,000 and attempting to defraud the ATO of a further $458,000, following a joint investigation by the Australian Federal Police (‘AFP’) and ATO’s serious financial crime taskforce. The investigation began in June 2020, after the ATO linked the man to several suspicious claims, including 40 fraudulent applications for JobKeeper. The sentence is “a warning to criminals who seek to exploit and steal from the Commonwealth and by extension, Australian taxpayers”.

New ATO guidance on “who is an employee?”

The ATO recently issued a ruling that explains when an individual is an ’employee’ of an entity for pay as you go (‘PAYG’) withholding purposes. A useful approach for establishing whether or not a worker is an employee of an engaging entity is to consider whether the worker is working in the business of the engaging entity, based on the construction of the terms of the relevant contract. Importantly, the fact that a worker may be conducting their own business, including having an ABN, is not determinative. More info on the ATO website here.

Editor: If you need help with this important issue, please contact our office.

UNPREDICTABLE INVESTMENT PREDICTIONS

Every year, we are inundated with investment predictions as the New Year approaches. While these forecasts often seem to be backed by economic data and historical trends, the reality is that most of them turn out to be incorrect.

The ever-changing nature of global investment markets, coupled with the sheer number of investors vying to make the best decisions, makes it extremely challenging to accurately predict the future.

Instead of trying to predict the future, the key lies in adhering to sound investment principles. At Hales Douglass Financial Services, we can assist you in developing and sticking to these principles, tailored to your specific needs and goals.

Whether it’s sustainable investing or traditional investment strategies, our philosophy is built on over decades of professional financial experience, detailed market research and a commitment to meeting your unique requirements.

By focusing on solid investment principles rather than attempting to forecast the unpredictable, you can set yourself up for long-term financial success.

At Hales Douglass Financial Services we’re here to provide the guidance and expertise you need to make informed decisions and build a robust investment portfolio and to help maintain your portfolio year after year. Contact Adam, Andrew, Jeanette or Cheyne for more information.

To read more, see Dimensional’s 2023 Market Review: Rising stocks left predictions grounded

TESTIMONIALS

Hales Douglass Financial Services

I cannot send enough gratitude your way, just for everything you have done and helped me with. I do not know where I would be if you had not made this all happen. It has relieved so much stress from my life, which means more than you can know.

Tieka Berry

High Definition Finance – loans

As first home buyers entering the housing market and purchasing our first home seemed extremely scary and nerve-racking, however, Ash has been absolutely amazing. Ash provided us with great options and guided us through our whole finance and purchase. Ash you’ve done the unthinkable for us and we can’t thank you enough. Highly recommend Ash & HD Finance.

Taylor Mizzi

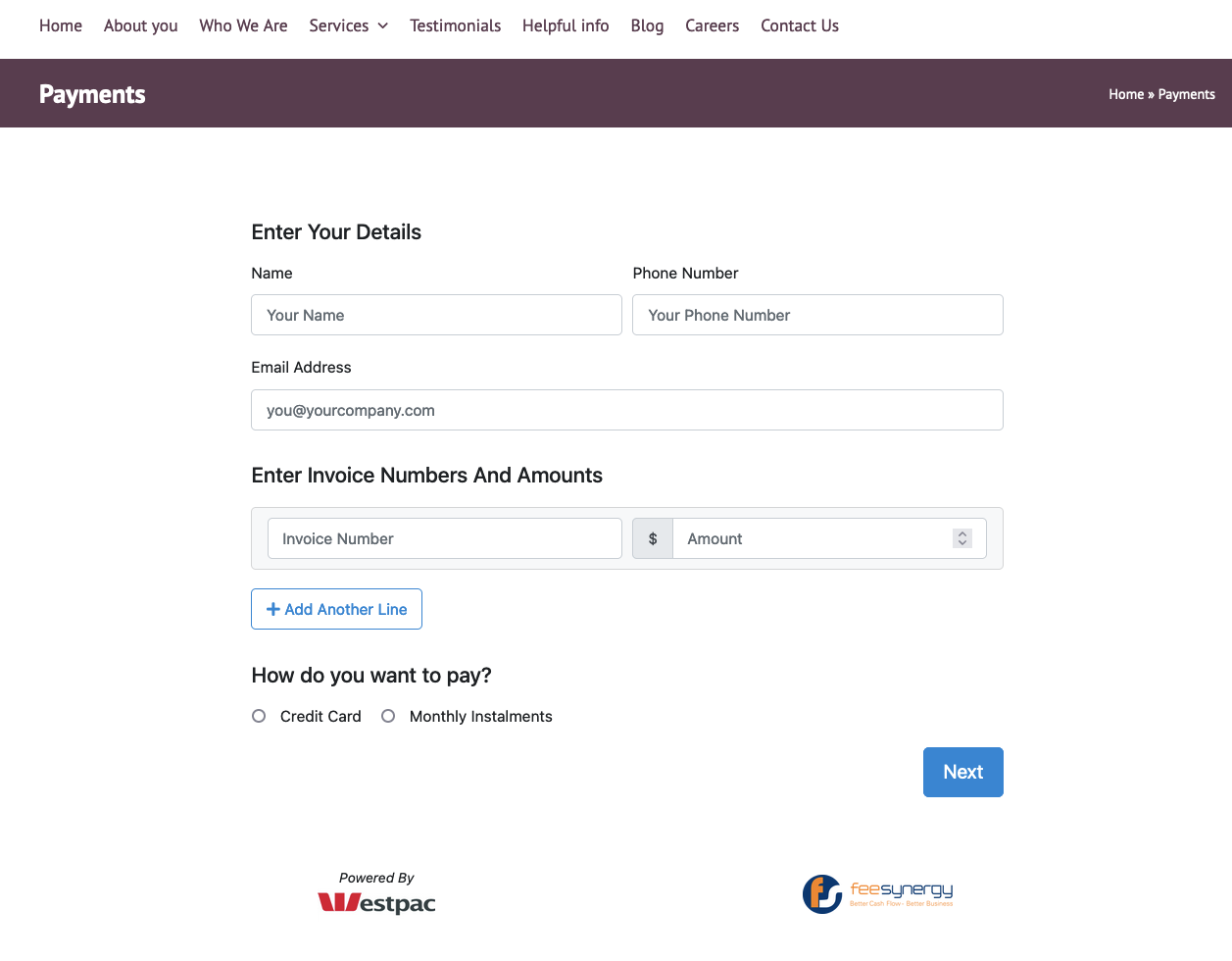

OUR NEW ONLINE PAYMENT LINK

We’ve created a new online payment link on our website, which incorporates state-of-the-art security, saves you time, and streamlines your payment experience.

The link is located on the top right-hand side of our home page when viewing on your desktop or laptop, or in the top middle when viewing on a mobile. You can choose to pay by credit card or by instalments.

MORE INFO?

For more information on any of these news stories, please email or call our office on (02) 4455 5333.

Please note: Many of the comments in this publication are general in nature and anyone intending to apply the information to practical circumstances should seek professional advice to independently verify their interpretation and the information’s applicability to their particular circumstances.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}